Bitcoin Miners Are Devouring Energy at a Record Pace During the Crypto Runup

By David Pan

After recovering from a near-death experience during the most recent crypto winter, Bitcoin miners are back in survival mode — spending billions of dollars on equipment and drawing energy at a record pace ahead of an update in the digital currency’s code that threatens revenue streams.

The surge in activity is sparked by a runup in the world’s largest cryptocurrency, fueled by newly launched spot Bitcoin exchange-traded funds, and a quadrennial event called the halving that is slated to take place in April. Bitcoin has surged more than fourfold since plunging by 64% in 2022 amid a series of crypto industry bankruptcies and scandals.

Since February 2023, 13 of the top mining companies have placed orders for over $1 billion worth of specialized computers, according to data compiled by TheMinerMag based on public filings. CleanSpark Inc. and Riot Platforms Inc. led the group, spending as much as $473 million and $415 million, respectively, on the rigs.

The machines are being purchased to help miners increase efficiency for their operations and lock in favorable electricity rates. Miners are in constant search of cheap power because they use energy-hungry computers to validate records of transactions on the blockchain to earn rewards in the form of Bitcoin.

“Scale matters because you can get machines for better rates, bigger energy deals and drive down the cost of development,” said Asher Genoot, chief executive at Hut 8 Corp., one of the largest publicly traded Bitcoin miners. “When you have scale, you have more marginal and growth profits and you can cover your big costs.”

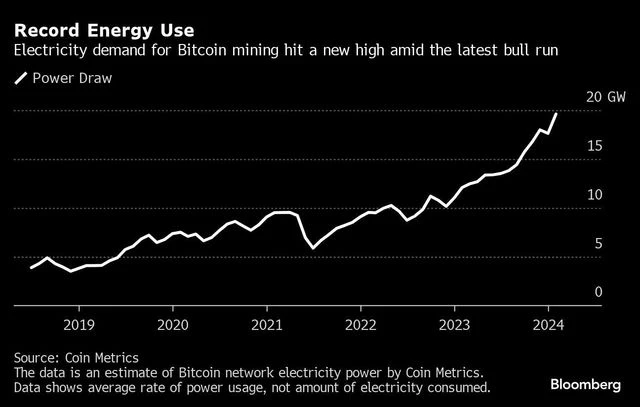

All the activity is driving miners to consume energy at a record pace. Last month, miners drew a record 19.6 gigawatts of power, up from 12.1 gigawatts the same period in 2023, according to an estimate by Coin Metrics. That’s equivalent to the electricity capacity that can power about 3.8 million homes in Texas, where many of the mining operations are located.

“If we assume power draw was consistent over the course of the month, we can multiply by 696 (24 hours times 29 days) to get 13.64 TWh (terawatt-hours) of energy consumed by the Bitcoin network over the course of last month,” said Coin Metrics Senior Solutions Engineer Parker Merritt. Bitcoin mining consumed 121 terawatt-hours of power in 2023, the Cambridge Centre for Alternative Finance estimates — similar to Argentina’s use.

"chart")

Bitcoin miners were some of the best performing stocks last year, allowing the companies to raise capital by selling newly issued shares through “at-the-market” offering programs. That’s in addition to the rising value of Bitcoin held on the books of the miners. Bitcoin reached a record high of more than $70,000 on March 8.

The rising price of Bitcoin “allows most miners to remain profitable,” said Zachary Bradford, CEO and president at CleanSpark, adding that his firm was profitable at lower prices.

Shares of Marathon and CleanSpark have risen by almost 600% and 900%, respectively, since December 2022. According to TheMinerMag data, both firms along with Riot, Hive Digital Technologies and Iris Energy Ltd. raised over $2 billion from selling shares since June 2023, when the crypto market started to rebound.

"chart")

“The most efficient miners will benefit the most as the increase in Bitcoin price will push even more profits to the bottom line,” said Bradford.

Miners are constantly competing for a reward since the network only gives it to the first to successfully process a unit of data. The fierce competition is evidenced in mining difficulty, a measure of the amount of computing power to mine Bitcoin. The bi-weekly gauge has posted some of the largest increases, pushing the figure to all-time highs several times since January 2023, according to data from btc.com.

The more computing power a miner has, the more likely it will get a reward. But that reward will be reduced after the halving, which further limits the supply of Bitcoin.

“With the halving coming in mid April, revenue for miners will fall significantly, forcing some of them into the territory of negative margins,” said Ethan Vera, chief operations officer at crypto-mining services provider Luxor Technology. “Some miners will capitulate, while many will find creative solutions to remain profitable.”

Danger of Scaling

The rapid expansion comes with risks as seen in the last crypto bull run in late 2021. A flurry of mining companies went public and raised billions of dollars from the equity and debt markets. Companies borrowed a record amount of money and when the market crashed in 2022 so did miners. Two of the largest firms at the time, Core Scientific Inc. and Compute North declared bankruptcy with other miners warning of a liquidity crunch. Core Scientific has since emerged out of bankruptcy and relisted in January.

“There is a danger in which you scale and start compromising on the cost of energy, the cost of machines and the costs of certain paybacks,” Genoot said. “That’s why so many companies went bankrupt in 2022 because people would scale at all costs.”

Phil Harvey, CEO at Sabre56, a large Bitcoin mining operator based in Dubai, said he knows a miner that has machines, worth $350 million or $400 million, that it purchased this year but has no where to put them.

The company has “no ability to turn them on,” he said. “That is not uncommon.”

First Published: Mar 09 2024 | 8:37 PM IST

Note:- (Not all news on the site expresses the point of view of the site, but we transmit this news automatically and translate it through programmatic technology on the site and not from a human editor. The content is auto-generated from a syndicated feed.))