Bitcoin extended its downturn, putting the coin on pace for a consecutive weekly decline as it gives back some of its 2023 gains.

Bitcoin, which pushed past $30,000 last month but was unable to hold that key level, has slipped about 10% so far in May.

So-called meme tokens — highly volatile coins that tend to go berserk during periods of heightened bullishness — have also given up recent gains, with daily trading volume dropping 50% to about $500 million from more than $1 billion, according to data from Kaiko.

“In part due to the extreme meme-coin phenomena lately, the major blockchains have become rather congested,” said Mati Greenspan, chief executive officer of Quantum Economics. “Transaction fees and confirmation times have gone up and most of the regular everyday users will probably prefer to wait until the network clears out before commencing their usual activities.”

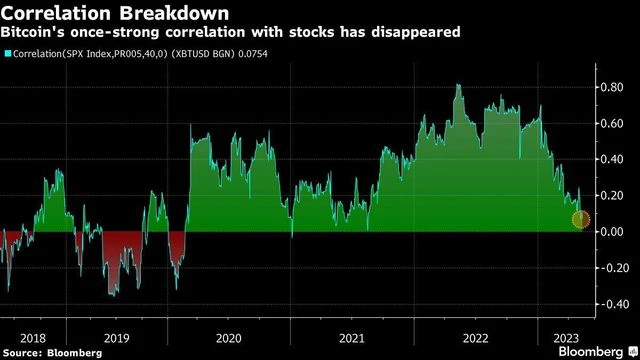

"chart")

Earlier this week it emerged that top market-making firms Jane Street Group and Jump Crypto are pulling back from trading digital assets in the US, while Jane Street is also scaling back its crypto ambitions globally.

Recent market swings have been driven largely by “spot selling, with derivatives data still not showing extremity of sentiment or positioning,” he added.

Analysts are now scouring for the next levels of support for Bitcoin. Markus Thielen, head of research at Matrixport, said he’d be “cautious and short until Bitcoin prices drop back to $24,600.”

Note:- (Not all news on the site expresses the point of view of the site, but we transmit this news automatically and translate it through programmatic technology on the site and not from a human editor. The content is auto-generated from a syndicated feed.))