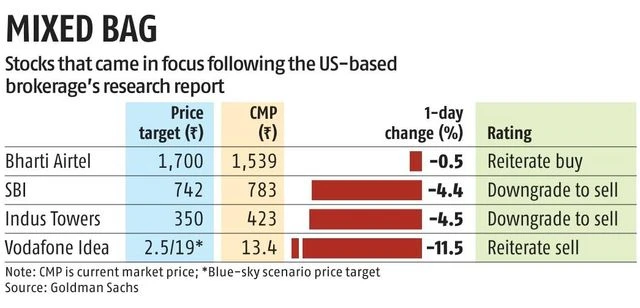

Goldman Sachs’ “sell” call on Friday sparked a decline in shares of State Bank of India (SBI), Indus Towers, and Vodafone Idea (VIL). However, Bharti Airtel’s shares proved resilient, dodging the broad-based selloff as the US-based brokerage reiterated its positive stance on the telecom major.

Goldman downgraded the country’s largest lender SBI, citing unfavourable risk-reward profile and risks to sustainability of return on assets (ROA). It said SBI’s loan growth could slow going forward given the widening gap between deposit growth and loan growth. Further, it expects an increase in credit costs on rising slippages in MSME, agriculture and unsecured portfolios. Shares of SBI fell 4.4 per cent to end at Rs 783. Goldman has lowered its price target from Rs 841 to Rs 742 for the stock, implying a 5.2 per cent downside from current levels. It has cut SBI’s FY25-27 earnings estimates by 3-9 per cent and target multiple to 1.0x from 1.2x of 12-month forward price-to-book.

"Chart")

Goldman has assigned a multiple of 9x on Indus’ projected 12-month forward EV/Ebitda (18x forward P/E). The stock currently trades at a 15 per cent discount from its 2015-18 average multiple, but 70 per cent higher than the stock’s last three-year average multiple, the brokerage noted.

VIL shares saw the maximum plunge of 11 per cent as Goldman assigned a base case target of Rs 2.5. It said the company’s recent fundraise is positive but may not be adequate to stem its market share erosion. The brokerage said as the capex spends of its peers could be at least 50 per cent higher, VIL could lose another 300 basis points (bps) market share over the next three-four years. It said VIL’s net debt-to-Ebitda could remain elevated at 19x by March 2025, which could put pressure on its balance sheet.

The brokerage, however, also assigned a “blue-sky scenario” price target of Rs 19, “where we assume 65 per cent lower AGR dues, consistent tariff increases and no near-term government repayments”.

Rival Bharti Airtel, on the other hand, earned accolades from Goldman, which saw its stock decline just 0.5 per cent even as the benchmark Sensex fell 1.24 per cent.

“Bharti Airtel’s execution in recent periods has been solid — wireless revenues have been consistently growing faster than that of peers, with the company gaining 250 bps of revenue market share in the last two years,” it said.

Goldman expects these tailwinds to sustain. It has raised Airtel’s FY25-30 Ebitda estimates for Bharti (India) by up to 32 per cent (consolidated Ebitda increase by up to 20 per cent).

While reiterating “buy”, it has increased the price target for the stock to Rs 1,700 from Rs 990 earlier, implying a 10 per cent upside from current levels.

First Published: Sep 06 2024 | 6:17 PM IST

Note:- (Not all news on the site expresses the point of view of the site, but we transmit this news automatically and translate it through programmatic technology on the site and not from a human editor. The content is auto-generated from a syndicated feed.))